Introduction to 401(k) Plans

A 401(k) plan is a retirement savings account offered by many employers to help employees save for their future. Named after a section of the U.S. Internal Revenue Code, these plans provide significant tax advantages that can help individuals build substantial retirement savings over time. By understanding and implementing effective strategies, you can maximize the benefits of your 401(k) and ensure a comfortable retirement.

Benefits of a 401(k) Plan

The primary benefit of a 401(k) plan is the ability to save for retirement in an advantaged manner. Contributions are made pre-tax, reducing your income for the year. Additionally, many employers offer matching contributions, essentially providing free money to bolster your retirement savings. 401(k) plans also benefit from compounding growth, which can significantly increase your savings over the long term.

Tax Advantages of 401(k) Contributions

One of the key benefits of a 401(k) plan is the advantage it offers. Contributions to a traditional 401(k) are made with pre-dollars, which lowers your income in the year you contribute. This deferral of taxes means you only pay taxes when you withdraw the money in retirement, ideally when you’re in a lower bracket. This deferral can result in significant tax savings over the years.

Understanding Employer Matches

Employer matching contributions are one of the most attractive features of a 401(k) plan. Employers typically match a percentage of the employee’s contribution, up to a certain limit. For example, an employer might match 50% of your contributions up to 6% of your salary. This match is essentially free money and a key component in growing your retirement savings. Always strive to contribute enough to get the full match from your employer.

Maximizing Your 401(k) Contributions

To make the most of your 401(k), aim to contribute the maximum amount allowed by the IRS. For 2024, the contribution limit is $19,500, with an additional catch-up contribution of $6,500 for those aged 50 and over. Contributing the maximum amount can significantly boost your retirement savings and take full advantage of the tax benefits.

Catch-Up Contributions for Those Over 50

If you’re over 50, you’re eligible to make catch-up contributions to your 401(k). This allows you to contribute an additional $6,500 in 2024, on top of the standard limit. Catch-up contributions are a great way to accelerate your savings as you approach retirement, ensuring you have enough funds to support your lifestyle in your later years.

Investment Options within a 401(k)

401(k) plans typically offer a range of investment options, including mutual funds, index funds, and company stock. Understanding these options and selecting a diversified mix that aligns with your risk tolerance and retirement goals is crucial. Diversification helps manage risk and can lead to more stable returns over time.

Diversification Strategies for 401(k) Investments

Diversification involves spreading your investments across different asset classes to reduce risk. In a 401(k) plan, this might mean allocating funds to a mix of stocks, bonds, and cash equivalents. By diversifying, you can protect your portfolio from significant losses if one particular investment performs poorly. Regularly review and adjust your asset allocation to maintain a diversified portfolio.

The Power of Compound Growth

Compound growth refers to the process where the earnings on your investments generate their earnings. This snowball effect can significantly increase your retirement savings over time. By starting your 401(k) contributions early and consistently investing, you can take full advantage of compound growth and build a substantial nest egg for retirement.

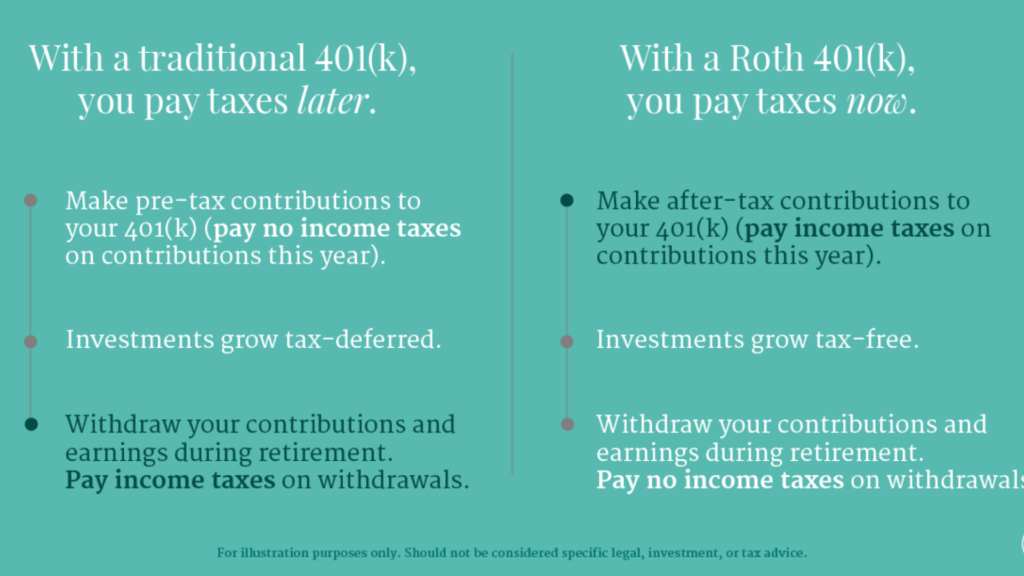

Roth 401(k) vs. Traditional 401(k)

A Roth 401(k) is an after-tax retirement account, meaning you pay taxes on contributions upfront, but qualified withdrawals in retirement are tax-free. In contrast, a traditional 401(k) offers tax-deferred growth, with contributions made pre-tax and withdrawals taxed as income. Choosing between the two depends on your current tax situation and expected tax bracket in retirement. Some investors opt for a combination of both to balance tax advantages.

Strategies for Tax-Efficient Withdrawals

Planning for tax-efficient withdrawals can help you minimize taxes in retirement. Consider withdrawing from taxable accounts first, followed by tax-deferred accounts, and finally tax-free accounts like a Roth 401(k). This strategy can help you manage your taxable income and reduce the overall tax burden on your retirement savings.

Avoiding Early Withdrawal Penalties

Withdrawals from a 401(k) before age 59½ are generally subject to a 10% early withdrawal penalty, in addition to ordinary income tax. To avoid these penalties, plan to leave your 401(k) funds untouched until you reach the appropriate age. If you must withdraw early, investigate exceptions to the penalty, such as using funds for significant medical expenses or a first-time home purchase.

Required Minimum Distributions (RMDs)

Once you reach age 72, the IRS requires you to start taking Required Minimum Distributions (RMDs) from your 401(k). RMDs are calculated based on your account balance and life expectancy. Failing to take your RMDs can result in a hefty penalty, so it’s essential to understand these requirements and plan accordingly to ensure compliance and minimize taxes.

Rolling Over Your 401(k) to an IRA

When you change jobs or retire, you might consider rolling over your 401(k) into an Individual Retirement Account (IRA). IRAs often offer more investment options and greater flexibility than 401(k) plans. Rolling over your 401(k) can be done tax-free if done correctly, allowing you to continue deferring taxes on your retirement savings.

Common Mistakes to Avoid with Your 401(k)

Avoiding common mistakes can help you make the most of your 401(k). These mistakes include not contributing enough to get the employer match, not diversifying investments, withdrawing funds early, and failing to increase contributions over time. By staying informed and proactive, you can avoid these pitfalls and ensure your 401(k) works effectively for your retirement goals.

How to Monitor and Adjust Your 401(k) Plan

Regularly monitoring your 401(k) plan and making adjustments as needed is crucial for long-term success. Review your account statements, assess your investment performance, and adjust your asset allocation to stay aligned with your retirement goals and risk tolerance. Periodic reviews can help you stay on track and make informed decisions about your retirement savings.

The Role of Financial Advisors in Managing Your 401(k)

A financial advisor can provide valuable guidance in managing your 401(k). They can help you develop a comprehensive retirement plan, choose appropriate investments, and optimize your tax strategy. Consulting with a financial advisor can give you peace of mind and ensure you’re making the most of your 401(k) plan.

Case Studies of Successful 401(k) Strategies

Examining case studies of successful 401(k) strategies can provide insights and inspiration for your own retirement planning. These examples often highlight the importance of early and consistent contributions, diversification, and taking full advantage of employer matches. Learning from others’ successes can help you implement effective strategies in your own 401(k) plan.

Frequently Asked Questions about 401(k) Plans

Addressing frequently asked questions about 401(k) plans can help clarify common concerns and provide valuable information. Topics might include contribution limits, employer matches, withdrawal rules, and the differences between Roth and traditional 401(k) accounts. Providing clear answers to these questions can empower you to make informed decisions about your retirement savings.

Conclusion and Final Tips for 401(k) Success

In conclusion, maximizing your 401(k) plan requires understanding its benefits, making informed contributions, and implementing tax-efficient strategies. By staying proactive, diversifying investments, and seeking professional advice when needed, you can grow your wealth and secure a comfortable retirement. Take full advantage of your 401(k) and watch your retirement savings flourish.