The Importance of Family Wealth Planning

In today’s complex financial landscape, effective family wealth planning is crucial for building and preserving wealth across generations. A strategic approach to managing finances ensures that family members are financially secure, educated about money matters, and prepared to handle future challenges. By setting clear goals and implementing well-thought-out strategies, families can create a robust financial foundation that supports both current and future generations.

Setting Financial Goals as a Family

The first step in family wealth planning is setting clear and achievable financial goals. These goals should reflect the family’s values and priorities, such as saving for a home, funding education, or planning for retirement. Involving all family members in this process fosters a sense of shared responsibility and commitment. Regularly reviewing and adjusting these goals ensures that they remain relevant and achievable as circumstances change.

Making and Following a Family Budget

A well-planned budget is the cornerstone of financial stability. Creating a family budget involves tracking income and expenses, identifying areas where spending can be reduced, and allocating funds toward savings and investments. Sticking to the budget requires discipline and regular monitoring to ensure that spending aligns with financial goals. Utilizing budgeting tools and apps can simplify this process and help maintain financial discipline.

Building an Emergency Fund for Financial Security

An emergency fund is essential for protecting the family against unexpected expenses such as medical emergencies, job loss, or major repairs. This money should ideally be sufficient to cover three to six months’ worth of living expenditures. Building an emergency fund requires consistent savings and may involve cutting back on non-essential expenses. This financial cushion provides peace of mind and ensures that the family can navigate unforeseen financial challenges without derailing long-term goals.

A Key Wealth Strategy

Investing in education is one of the most impactful ways to build and preserve wealth. Education opens doors to better job opportunities, higher incomes, and financial stability. Families should prioritize saving for children’s education through dedicated savings accounts or education savings plans. Additionally, promoting lifelong learning among all family members can enhance skills and adaptability in an ever-changing job market.

Diversifying Investments for Long-Term Growth

A key idea in investing that helps minimize risk and optimize returns is diversification. Families should consider a mix of asset classes, such as stocks, bonds, real estate, and mutual funds. Diversifying investments across different sectors and geographic regions further reduces risk. Regularly reviewing and rebalancing the investment portfolio ensures that it aligns with the family’s financial goals and risk tolerance.

Ensuring Wealth Transfer Across Generations

Estate planning is critical for ensuring that wealth is transferred smoothly and efficiently to the next generation. Making a will, setting up trusts, and naming beneficiaries for life insurance and retirement savings are important aspects of estate planning. Proper estate planning minimizes legal complications, reduces estate taxes, and ensures that assets are distributed according to the family’s wishes.

Tax Planning and Efficient Tax Strategies

Effective tax planning can significantly enhance a family’s wealth-building efforts. Strategies such as utilizing tax-advantaged accounts, taking advantage of deductions and credits, and planning for capital gains can reduce tax liabilities. Consulting with a tax advisor helps identify the most effective tax strategies based on the family’s financial situation and goals.

Protecting Family Assets and Income

Insurance is a vital component of family wealth planning, protecting against financial loss due to unforeseen events. Property, life, health, and disability insurance are important categories of insurance. Adequate insurance coverage ensures that the family’s assets and income are protected, providing financial stability and peace of mind.

Teaching Financial Literacy to Children

Teaching financial literacy to children prepares them for a lifetime of sound financial decision-making. Families can start by educating children about basic financial concepts such as saving, budgeting, and investing. Encouraging children to manage their own money through allowances or part-time jobs fosters responsibility and financial independence. Financially literate children are better equipped to build and preserve wealth as they grow older.

Real Estate Investments as a Family Wealth Strategy

Real estate investments can provide steady income and long-term capital appreciation. Families can invest in rental properties, commercial real estate, or real estate investment trusts (REITs). Proper research and due diligence are essential for making informed real estate investment decisions. Diversifying real estate holdings across different markets and property types further enhances the potential for growth and stability.

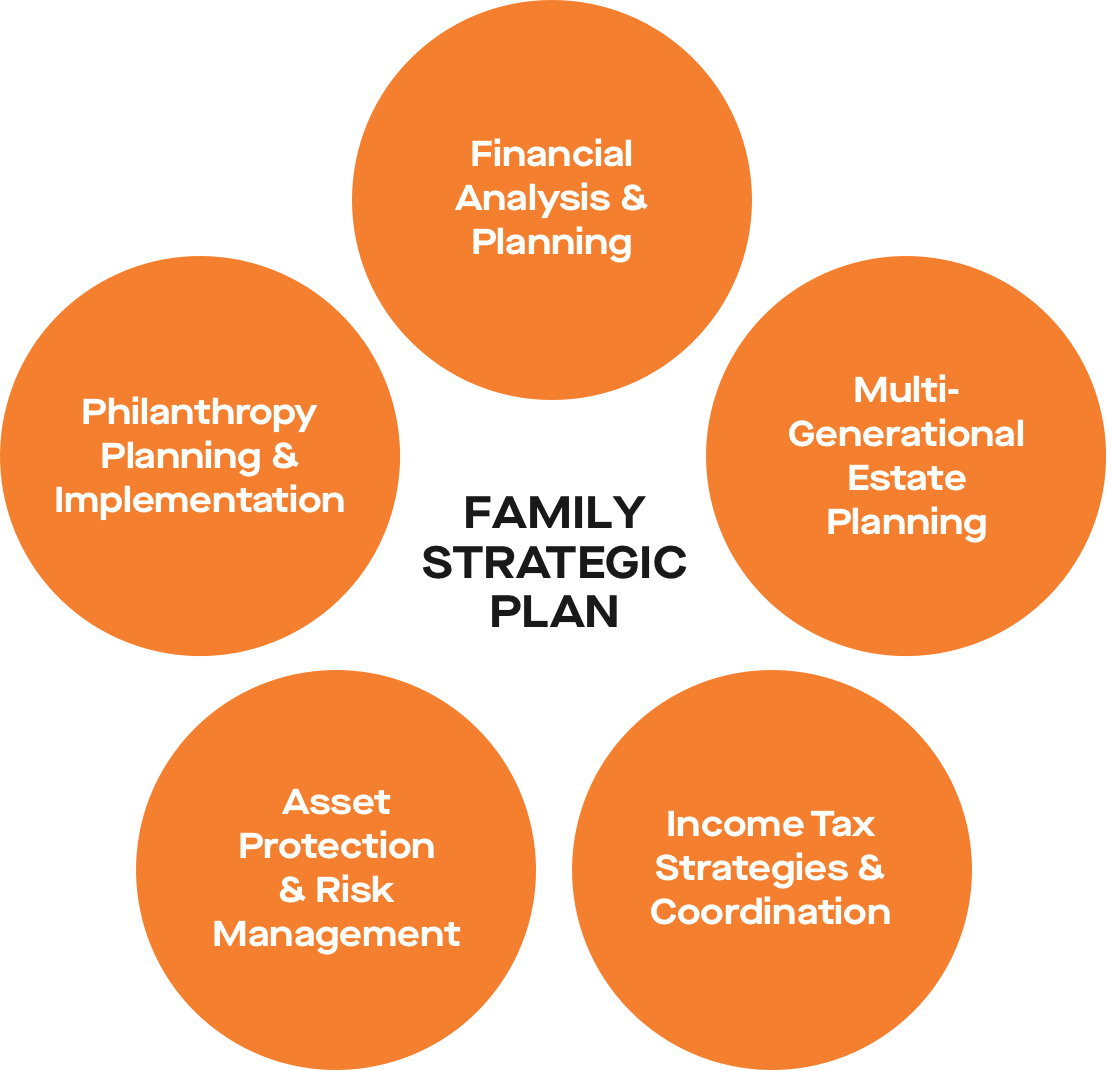

Strategies for Multi-Generational Planning

Retirement planning is a critical aspect of a family wealth strategy. Families should consider contributing to retirement accounts such as 401(k)s, IRAs, or pensions. Multi-generational planning involves coordinating retirement savings strategies among family members to ensure financial security for both current and future retirees. Starting retirement savings early and maximizing contributions can significantly enhance retirement outcomes.

Charitable Giving and Its Role in Wealth Preservation

Charitable giving not only supports causes that align with family values but also offers tax benefits and enhances the family’s legacy. Families can establish charitable foundations, and donor-advised funds, or make direct donations to non-profits. Incorporating charitable giving into the wealth strategy fosters a sense of purpose and social responsibility while preserving wealth through tax-efficient giving.

Using Trusts and Legal Instruments for Wealth Management

Trusts and other legal instruments are powerful tools for managing and preserving family wealth. Trusts can provide for minor children, protect assets from creditors, and manage estate taxes. Different types of trusts, such as revocable, irrevocable, and charitable trusts, serve various purposes. Consulting with an estate planning attorney ensures that the appropriate legal instruments are in place to meet the family’s financial objectives.

The Role of Professional Advisors in Family Wealth Planning

Professional advisors, including financial planners, tax advisors, and estate planning attorneys, play a crucial role in family wealth planning. These experts provide guidance on investment strategies, tax planning, estate planning, and more. Working with trusted advisors ensures that the family’s financial plan is comprehensive, up-to-date, and aligned with their goals.

Monitoring and Adjusting Family Financial Plans

Regularly monitoring and adjusting the family financial plan is essential for staying on track. Changes in income, expenses, market conditions, and family dynamics can impact financial goals. Conducting annual reviews and making necessary adjustments ensures that the financial plan remains relevant and effective.

Navigating Financial Challenges and Uncertainties

Families may face financial challenges such as economic downturns, job loss, or unexpected expenses. Having a well-thought-out financial plan and an emergency fund helps navigate these uncertainties. Flexibility, resilience, and a proactive approach to managing finances enable families to overcome challenges and stay on course toward their financial goals.

Case Studies

Examining successful family wealth strategies provides valuable insights and inspiration. Case studies of families who have effectively built and preserved wealth highlight the importance of planning, discipline, and adaptability. These examples demonstrate how different strategies can be tailored to meet unique family needs and circumstances.

Common Mistakes in Family Wealth Planning

Avoiding common mistakes is crucial for successful wealth planning. Common pitfalls include lack of planning, inadequate insurance coverage, failing to diversify investments, and neglecting to update the financial plan. Learning from these mistakes and implementing best practices enhances the likelihood of achieving financial success.

Conclusion

Building and preserving family wealth requires a comprehensive, strategic approach. By setting financial goals, creating a budget, investing wisely, and planning for the future, families can achieve financial security and stability. Embracing a proactive and disciplined approach to wealth management ensures that the family’s financial legacy is protected and preserved for generations to come.